Eurex Clearing

1. Introduction

The stress period Value-at-Risk (VaR) is an integral part of Eurex Clearing’s Prisma methodology. To mitigate potential pro-cyclical behavior of initial margins, the stress period VaR serves as a prudent margin floor primarily relevant during low volatility market regimes. Model parameters comprise the selection of historical stress period dates for the risk scenarios and the quantile level on which the margin floor is evaluated and which is calibrated to match a long-term target VaR.

As part of regular annual review, Eurex Clearing recalibrated the stress period parameters used in the Prisma model for margining of Exchange Traded Derivatives (ETD) and Over-The-Counter Derivatives (OTC).

Effective 16 June 2025, for all liquidation groups, the annual recalibration will affect the following model parameters (see both tables under 3.):

The recalibrated parameters are included in this circular and will be incorporated in the transparency enabler files on the effective date.

Production start: 16 June 2025

2. Required action

There are no required actions or infrastructure changes for participants. The margin model parameter revision will be automatically reflected in the required initial margin amounts at the start of business on the production start date. All model parameters are distributed in the usual manner as part of the current Member reporting (reports CC221, CC202).

3. Details of the initiative

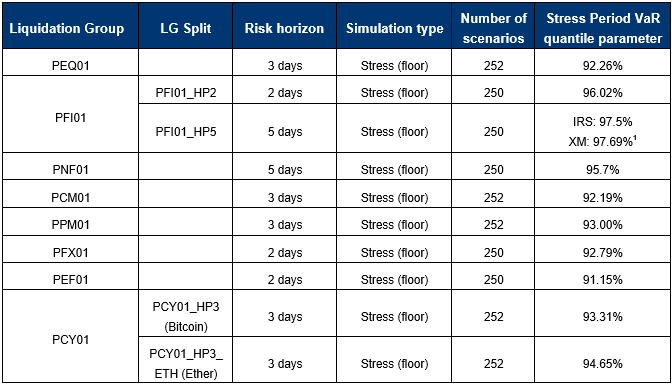

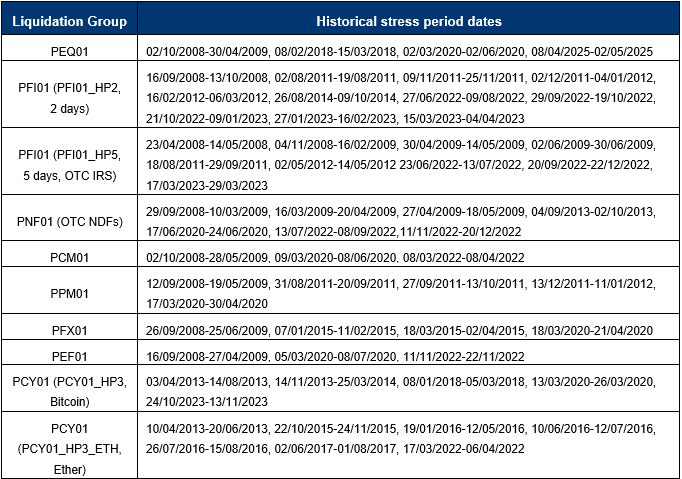

Please refer to the tables below which summarize the relevant Stress Period VaR parameters for all liquidation groups:

1 The Stress Period VaR confidence level parameters differ between OTC IRS only accounts and XM (cross margining) activated accounts purely for technical reasons. The resulting margin floor values embedded in Prisma Initial Margin model are equivalent.

Unless the context requires otherwise, terms used and not otherwise defined in this circular shall have the meaning ascribed to them in the Clearing Conditions or FCM Clearing Conditions of Eurex Clearing AG, as applicable.

Further information

Recipients: | All Clearing Members, ISA Direct Clearing Members, Disclosed Direct Clients of Eurex Clearing AG and vendors, all FCM Clearing Members and other affected contractual parties | |

Target groups: | Front Office/Trading, Middle + Backoffice, IT/System Administration | |

Contact: | Your Clearing Key Account Manager or client.services@eurex.com | |

Web: | www.eurex.com/ec-en/ | |

Authorized by: | Dmitrij Senko |